How Does This War End?

EXECUTIVE SUMMARY

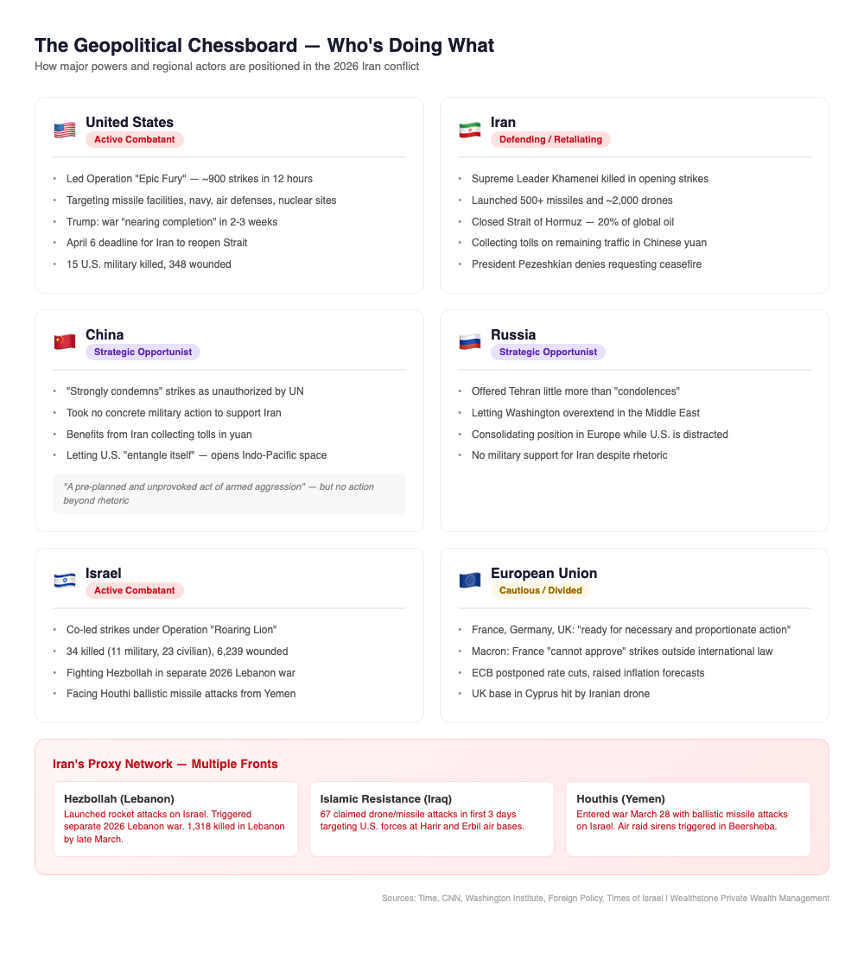

On February 28, 2026, the U.S. and Israel launched Operation “Epic Fury” against Iran, killing Supreme Leader Khamenei and dozens of senior military and political figures in roughly 900 airstrikes over 12 hours. Iran retaliated not with conventional military force, but with economic warfare: closing the Strait of Hormuz, activating regional proxies, and launching 500+ missiles and 2,000 drones at Israel, U.S. bases, and Gulf states.

The economic fallout is severe and accelerating. Brent crude surged 45% in 30 days to $105/barrel, the largest monthly gain since Brent’s inception in 1988. U.S. gasoline hit $4.00/gallon. European natural gas jumped over 50%. Global shipping rates are up 150%. Goldman Sachs raised its U.S. recession probability to 30%; EY-Parthenon puts it at 40%.

The geopolitical chessboard favors China and Russia in the near term. Both nations’ ships transit the Strait freely. China is buying discounted Iranian oil. Russia has extracted partial sanctions relief and is pushing for permanent commitments before selling oil to Europe. The U.S. strategy of regime change has failed; Iran’s new power brokers are more hostile, not less.

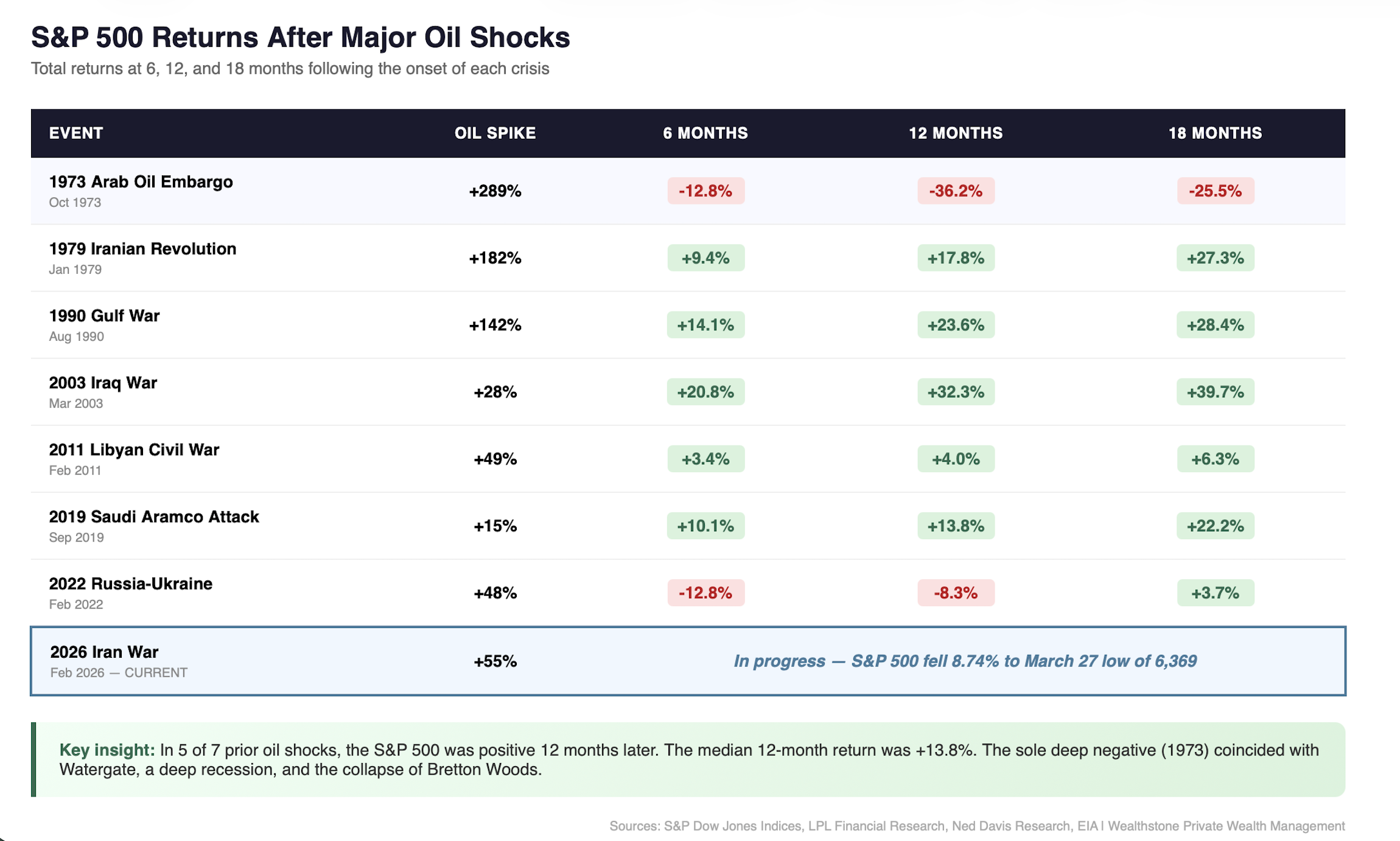

History says be patient. In five of seven prior oil shocks, the S&P 500 was positive 12 months later, with a median return of +13.8%. But inflation is the wildcard: if oil stays above $100 for months, stagflation risk becomes real. I expect the negative market impact from this war to subside before a formal peace deal is reached, but between now and then, a lower-risk posture is warranted.

My base case: the U.S. will be forced to negotiate with Iran’s current government, likely through an intermediary such as China or Pakistan, within 2 to 6 months. The economic pain is too large to sustain. The outcome will favor Iran more than the U.S., because Iran holds the economic cards right now.

THE ATTACK AND IRAN’S RESPONSE

On February 28, 2026, the U.S. and Israel launched the most consequential military strike since the Iraq War. Operation “Epic Fury” delivered roughly 900 airstrikes in 12 hours, eliminating Supreme Leader Khamenei along with a long list of Iran’s top military and political leaders (DoD briefings, February 28 to March 1).

Iran’s response was immediate. In retrospect, it was brilliant.

The Iranians were never going to win a conventional war against the United States. Both nations have war-gamed this scenario since 1979. Iran knew the playbook. So instead of fighting a losing military conflict, they launched an economic assault on the entire world. Within hours, Iran fired 500+ missiles and approximately 2,000 drones at Israel, U.S. military bases, and Gulf states. But that was the distraction. The real weapon was economic.

On March 4, Iran shut down the Strait of Hormuz.

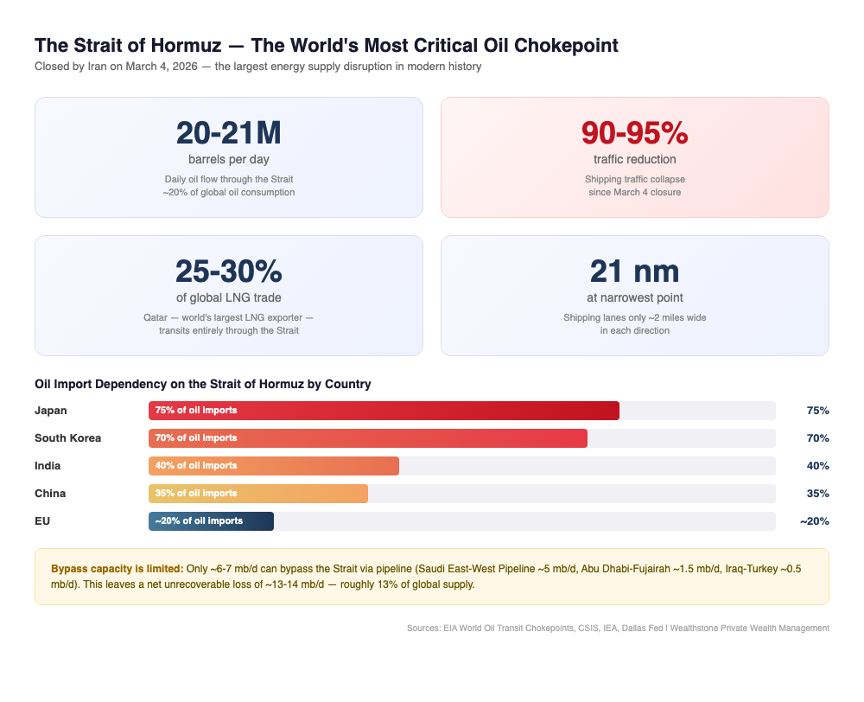

THE STRAIT: WHY IT CHANGES EVERYTHING

Source: Wealthstone Private Wealth Management

This is where the math gets brutal. The Strait of Hormuz handles 20 to 21 million barrels of oil per day, roughly 20% of global consumption. It also carries 25 to 30% of the world’s LNG trade. Since the closure, traffic through the Strait has dropped 90 to 95% (EIA, IEA).

The exposure is enormous. Japan relies on the Strait for 75% of its oil imports. South Korea, 70%. India, 40%. China, 35%. The bypass capacity (pipelines that can route around the Strait) tops out at 6 to 7 million barrels per day (EIA). That leaves a gap of roughly 14 million barrels per day with no alternative route.

For scale: this is the largest supply disruption in modern history. The next-largest was the 1979 Iranian Revolution, which removed 5.6 million barrels per day, or 8.9% of global supply (IEA historical data). The 2026 closure has knocked out more than three times that volume. Nothing else comes close.

Iran does not even need to physically block every ship. Cheap drones, kamikaze boats, and mines make it nearly free to keep the Strait closed. But the real lever is insurance. Underwriters have already begun canceling coverage on the multi-billion-dollar tankers that would need to transit. No insurance means no transit, regardless of whether a ship could physically get through. The Strait is closed by economics as much as by military threat.

And Iran is playing another card. The ships that do pass through, Chinese and Russian vessels primarily, are paying tolls. In Chinese yuan. Not dollars (regional shipping monitors and financial press reporting).

THE ECONOMIC DAMAGE

Oil and Energy: Brent crude surged from $72.48 to $105 per barrel in 30 days, a 45% increase and the largest monthly gain since Brent began trading in 1988. WTI hit $100.12. U.S. gasoline jumped from $2.92 to $4.00 per gallon (EIA, Bloomberg).

European Natural Gas: Prices are up over 50% since the war began. The ECB has postponed planned rate cuts. Europe’s economy, already fragile, is heading for a serious slowdown (ECB, European energy exchange data).

Inflation Transmission: The chain reaction is straightforward. Strait closed. Oil up 45%. Shipping rates up 150%. Fertilizer prices up 40%. Food and consumer prices rising across the board. The OECD now forecasts U.S. inflation at 4.2%. The UK is expected to breach 5%. EU estimates range from 2.6% to 4.4%. Inside Iran, food inflation has hit 105% (OECD, national statistical agencies).

Shipping and Trade: Global shipping rates have increased 150%. Rerouting cargo around the Strait adds 10 to 14 days to Asia to Europe routes. The cost structure for moving goods globally changed overnight (Freightos, Drewry Shipping Index).

Recession Risk: Goldman Sachs raised its U.S. recession probability to 30%, up from 15% pre-war. EY-Parthenon puts it at 40%, up from 35% (Goldman Sachs Global Research, EY-Parthenon).

Federal Reserve Impact: Before the war, markets expected two rate cuts in 2026. Now, only one is priced in. The Fed held rates at 3.50 to 3.75% in March. The 10-Year Treasury sits at 4.46%. The 30-year mortgage rate has climbed to 6.38%. PCE inflation forecasts have been raised to 2.7% (Federal Reserve, CME FedWatch).

Global Markets: The S&P 500 fell to a 2026 low of 6,369 on March 27 (down 4.6% for Q1 and 8.74% from its January highs), before recovering to ~6,582 by early April. The Nasdaq fell nearly 13% from its record high, entering correction territory. The Dow entered correction territory, falling over 10% from highs. On March 27 alone, the Dow dropped nearly 800 points to close at 45,167, capping five consecutive weekly losses. Internationally, the damage is worse: South Korea’s KOSPI dropped 12%, triggering circuit breakers. Pakistan’s KSE fell 9.6%. Thailand dropped 8%. Japan’s Nikkei lost over 2%. JPMorgan cut its S&P 500 year-end target from 7,500 to 7,200 (Bloomberg, Reuters, exchange data).

Source: Wealthstone Private Wealth Management

The SPR Response: In the largest coordinated release in history, the IEA organized 400 million barrels from 30+ nations, with the U.S. contributing 172 million barrels, bringing the U.S. SPR to a three-decade low. This buys time. It does not solve the supply problem (IEA, DOE).

Everything hinges on duration. If this war truly ends in 2 to 3 weeks, as the President continues to promise, with an April 6 deadline for Iran to reopen the Strait, the damage will be painful but manageable. If it drags on for months, like the war in Ukraine, we are looking at a global recession and a fundamental shift in the world order, as China and Russia end up calling the shots in this region.

THE GEOPOLITICAL CHESS MATCH

Source: Wealthstone Private Wealth Management

When I analyze geopolitical conflicts, I focus on two things. First, the chess match: the strategic moves and counter-moves between the world’s major powers, today, that is the U.S., China, and Russia. Second, the economic pressure, because the tipping point that pushes a regional war into something larger is how badly the conflict damages the economies of major nations. No country will sit still while its economy slides into depression. Governments facing that kind of pressure would rather go to war than lose power through protests, referendums, or revolution.

Here is what the board looks like right now.

The U.S. and Israel: The strategy was to create enough chaos in Iran combined with the January protests, in which Iranian security forces killed thousands of their own citizens, to topple the regime and replace it with leadership friendlier to U.S. and Israeli interests. That strategy has failed. Power brokers inside Iran have consolidated control. The new leadership is more anti-American than the last. U.S. casualties stand at 15 killed and 348 wounded. The human cost is real. The strategic objective is unmet (DoD, CENTCOM).

China: Beijing is the clearest winner so far. Chinese ships transit the Strait freely. China is buying Iranian oil at a discount. It has issued statements “strongly condemning” the strikes while doing nothing to stop the war, because the war serves Chinese interests. The U.S. is spending billions, burning through missile defense inventory, and potentially committing tens of thousands of troops to a ground war. Every dollar and every asset the U.S. spends in Iran is a dollar and an asset not available for the Pacific (CSIS, open-source intelligence reporting).

Russia: Moscow is also winning. Russian ships pass through the Strait without issue. The global oil shortage has forced the U.S. to reduce or temporarily remove sanctions on Russian oil, allowing other nations to buy it during this crisis, directly funding the same war machine the U.S. and Europe are fighting in Ukraine. Russia has gone further: it is demanding that countries commit to not re-imposing sanctions as a condition of selling oil to Europe, effectively locking those nations out of future alignment with the U.S. (Reuters, European diplomatic reporting).

The Casualties: The total human cost through early April: Iran has suffered 2,076+ killed and 26,500 wounded. Israel has lost 34 killed with 6,239 wounded. Lebanon reports 1,318 killed and 3,935 wounded. Across the conflict, more than 3,470 people have been killed and 37,000 wounded. Over 4,000 flights are being canceled daily across the region (regional health ministries, flight tracking data).

HOW I THINK THIS ENDS

The U.S. could continue eliminating Iranian leaders until someone sympathetic to American interests takes charge. But that outcome is not guaranteed, and the cost of getting there may exceed anything gained from it.

The middle ground is where this is heading.

The ground assault question: The U.S. may initiate a ground operation in the coming days or weeks. The strategic target would be Kharg Island, Iran’s economic lifeblood and the source of most of its oil exports. But this operation has been discussed publicly for weeks. That concerns me. This could become a Bay of Pigs situation, U.S. troops and assets sent into a fight the enemy has had weeks to prepare for. If the attack fails, the President faces three options: double down by sending more troops and committing to a long-term war, walk away after a failed assault (unlikely, given this administration), or reveal the entire buildup as a negotiation tactic designed to pressure Iran. I believe a ground assault will happen, despite the White House and other commentators denying it.

The endgame: The Iranian government is not going to be toppled. That reality narrows the options. The U.S., likely through an intermediary such as China or Pakistan, will have to cut a deal with Iran’s current leadership. The economic fallout may become so severe that the U.S. simply returns to the status quo that existed before the attack.

I agree with a growing number of analysts on this: the justification for this war appears flawed, most Americans do not support it, and it likely ends with us returning to roughly where we started, which, by any honest measure, is a strategic loss for the United States. I believe the economic damage over the next 2 to 6 months will force the U.S. to step away from this conflict or risk fracturing long-standing alliances.

Oil price scenarios support this timeline. A quick resolution could bring Brent back to $70 to $80 by Q3. A protracted conflict keeps it at $85 to $95 through late 2026. Escalation pushes it to $120 to $150+, at which point a global recession becomes nearly certain (Goldman Sachs, Morgan Stanley, energy analyst consensus).

WHAT THIS MEANS FOR MARKETS AND PORTFOLIOS

Source: Wealthstone Private Wealth Management

The historical data on oil shocks and wars is clearer than most people think.

Oil shocks and markets: In five of seven prior oil shocks, the S&P 500 was positive 12 months later. The median 12-month return was +13.8%. The 1979 Iranian Revolution saw the S&P return +17.8% over the following year. The 1990 Gulf War: +23.6%. The 2003 Iraq War: +32.3%. The sole deeply negative outcome, the 1973 shock, coincided with Watergate, a constitutional crisis layered on top of the oil shock (S&P Global, Bloomberg historical data).

Markets during wars: The S&P 500 rose during four of the five major U.S. military conflicts in the modern era. The exception was 2001 to 2003, driven by the dot-com bust, not the war itself.

Defense sector: Defense stocks surged immediately: Northrop Grumman gained 6% the day after the attack, Raytheon 4.7%, Lockheed Martin 3.4%. The sector is up 40% year-to-date. Lockheed is quadrupling THAAD missile production. Raytheon is scaling Tomahawk production 2 to 4x. If you own defense exposure, hold it (Bloomberg, company filings).

The gold paradox: Gold is declining during this war, the worst wartime gold performance on record. The logic: rising oil drives inflation fears, which push Treasury yields higher, which strengthens the dollar, which pressures gold. Gold outperformed in six of eight prior geopolitical crises. This time is the exception, and it is catching many investors off guard (World Gold Council, Bloomberg).

My positioning view: I expect the negative market impact from this war to fade before a formal ceasefire or peace deal is reached. Markets price in the future, and once uncertainty begins to recede, even slightly, buyers will step in. History supports this. But between now and that inflection point, anything can happen. A failed ground assault, an escalation drawing in other nations, a prolonged Strait closure; any of these could extend the pain.

For clients, I am recommending a lower-risk posture right now. A larger-than-usual cash position is not a drag when the market is flat or declining. Energy and defense names are outperforming. Tech and consumer discretionary are absorbing the most damage. The opportunity to buy aggressively will come, but I want to buy when uncertainty is subsiding, not while it is still building.

The inflation question is the wildcard. If oil stays above $100 for an extended period, the Fed’s hands are tied, rate cuts get pushed further out, and stagflation risk becomes real. That shifts this from a temporary shock to a structural problem. I am watching the oil curve and the Fed’s language closely.

THE BOTTOM LINE

The U.S. will reach a deal with Iran. It will not be what either side wants. But the deal will favor Iran more, because they hold the economic cards. The Strait of Hormuz is the most powerful bargaining chip on the table, and Iran is playing it well.

The U.S. and Israel will have to rethink how they address Iran’s influence in the region. This will not be the last conflict of this kind in our lifetime.

For investors: stay disciplined, stay patient, and be ready to act when the fog starts to lift. The historical record strongly favors those who hold through these periods, but risk management matters in the interim.

I will continue to update clients as this situation evolves.

Zak Gardezy, CFP®

Founder & Private Wealth Advisor

Wealthstone Private Wealth Management

Sources referenced in this analysis: U.S. Energy Information Administration (EIA), International Energy Agency (IEA), Federal Reserve, Department of Energy (DOE), Department of Defense (DoD), CENTCOM, Goldman Sachs Global Research, EY-Parthenon, S&P Global, Bloomberg, Reuters, OECD, World Gold Council, European Central Bank (ECB), CSIS, CME FedWatch, Wells Fargo Investment Institute, Freightos, Drewry Shipping Index, company filings, regional health ministries, and open-source intelligence reporting.

Disclaimer: This commentary reflects the personal views of Zak Gardezy as of April 2, 2026. It is intended for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal. Clients should consult with their advisor before making any portfolio changes.